")

Mortgage

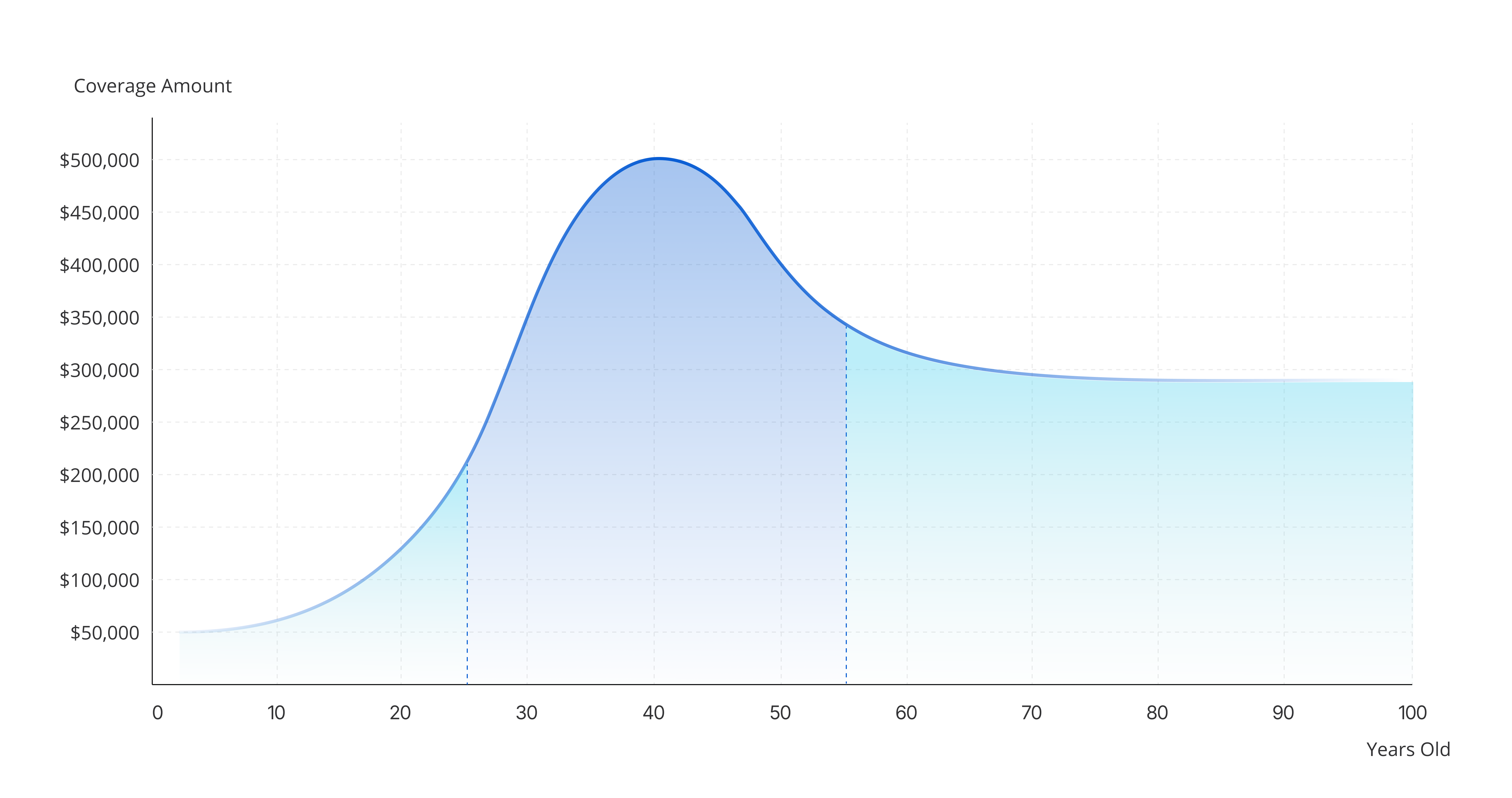

A mortgage is a substantial financial commitment, and if you were to pass away, your family might be left with the responsibility of continuing mortgage payments.

Household Expenses

Guarantee that your family can sustain their existing lifestyle, covering day-to-day expenses such as housing costs, utilities, groceries, transportation, and other routine expenditures.

College Expenses

Ensure adequate financial support for your dependents' education in the event of your death.

Any Other Debts

You’ll want to ensure that the policy's death benefit can cover outstanding financial obligations and prevent a burden on your beneficiaries.

Final Expenses

You may want to be sure that there are funds available to cover funeral and burial costs, relieving your family of the financial burden associated with end-of-life arrangements.

$175,000

to pay off his house

+

$90,000

for future college costs

+

$20,000

for his vehicles

+

$7,000

for funeral and burial

+

$5,000

for credit card bills

=

$297,000

IN TOTAL EXPENSES

")

")