How Much Life Insurance Do I Need?

Your Life Insurance coverage needs are as unique as you are.

At AmFi, we believe life insurance should be tailored to each individual based on their specific financial circumstances, responsibilities, and future plans.

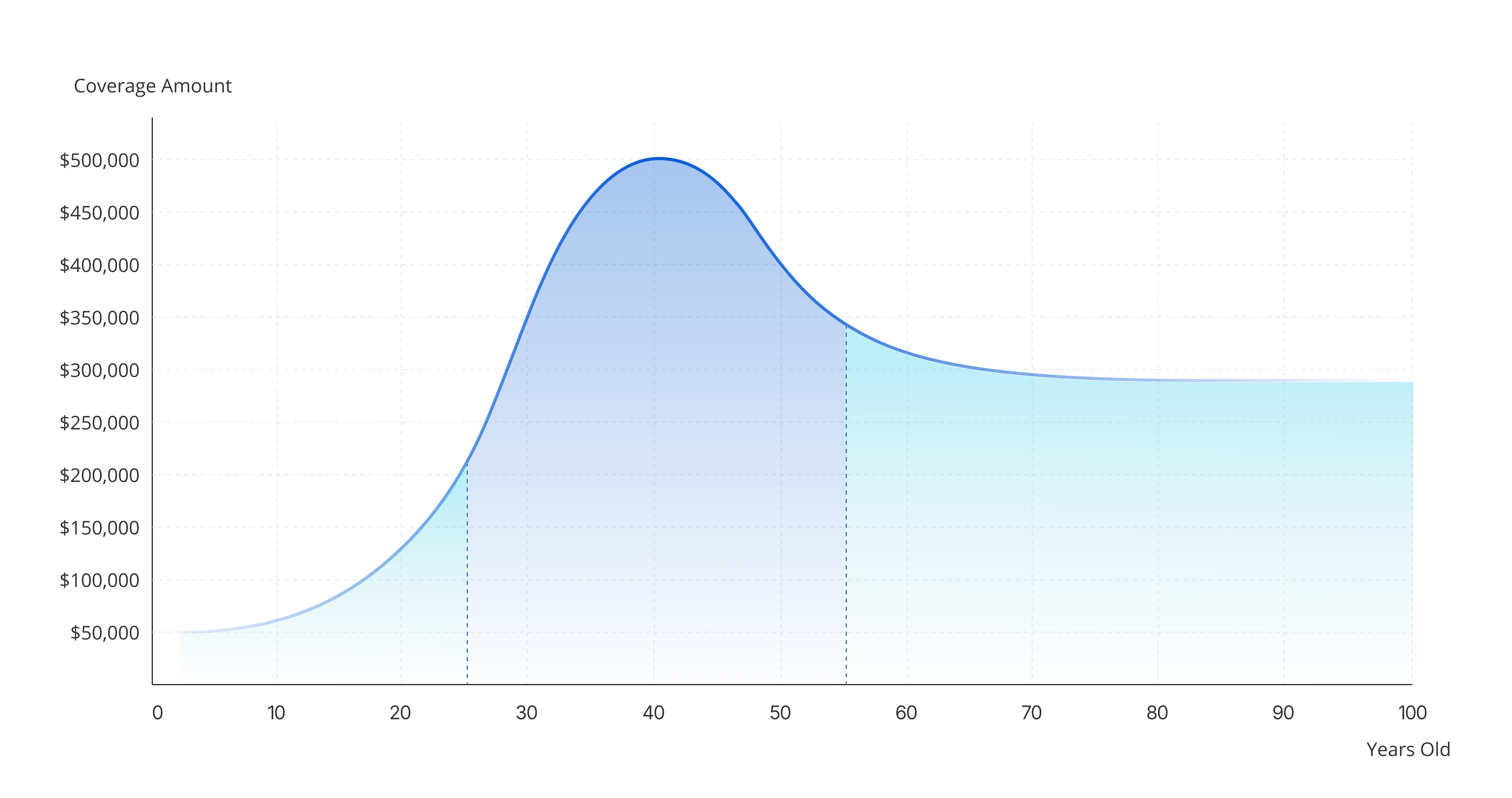

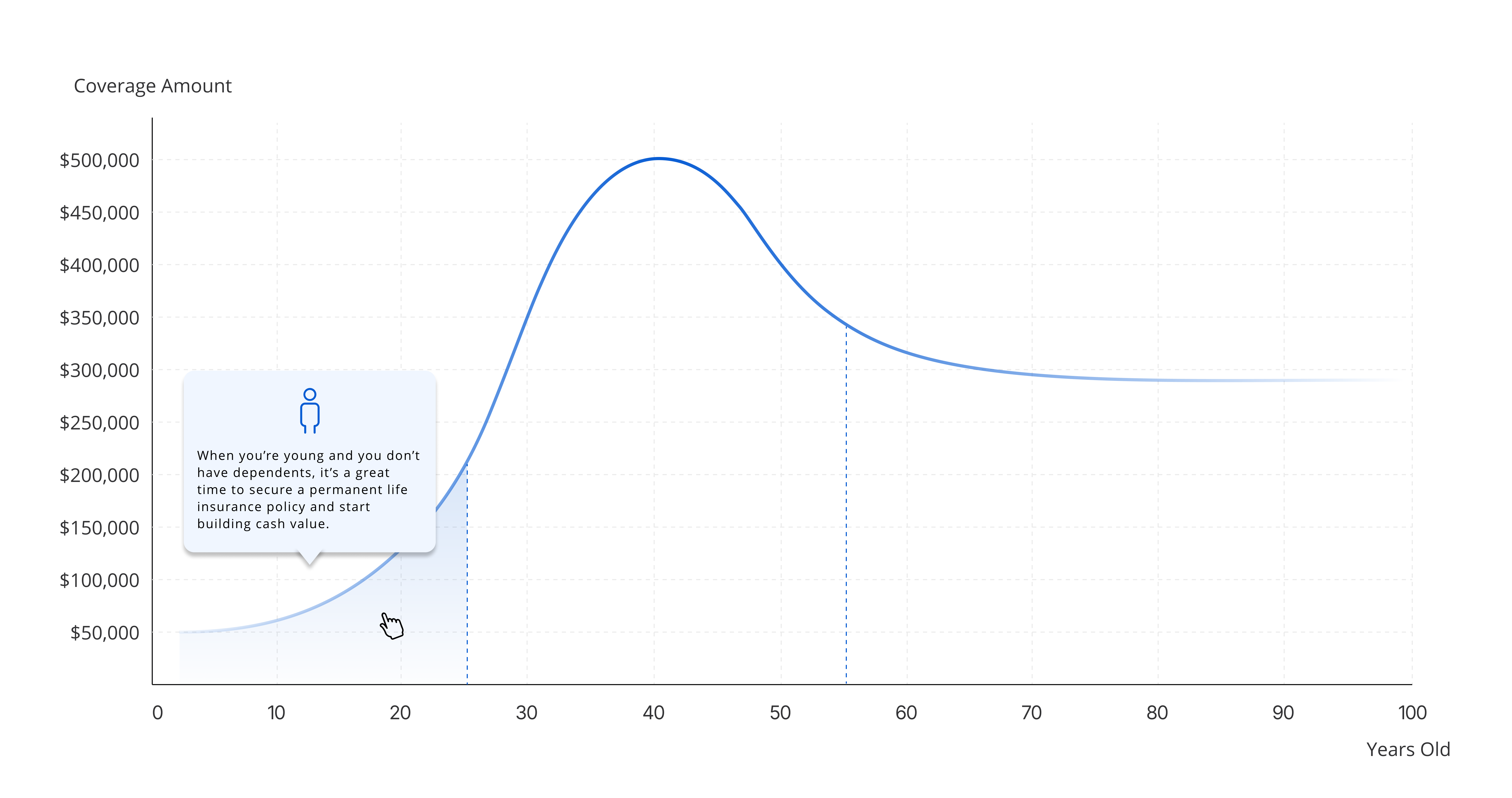

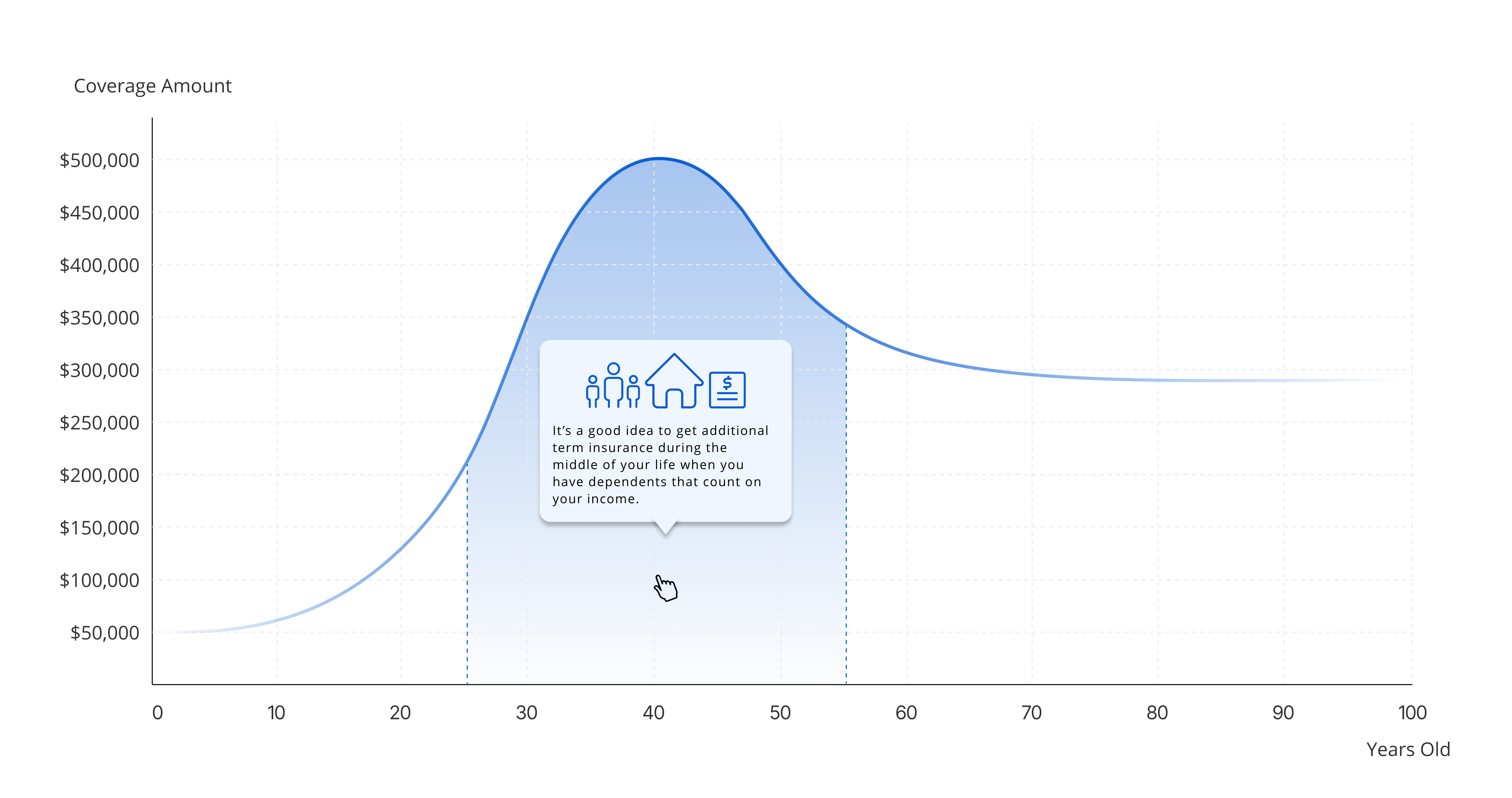

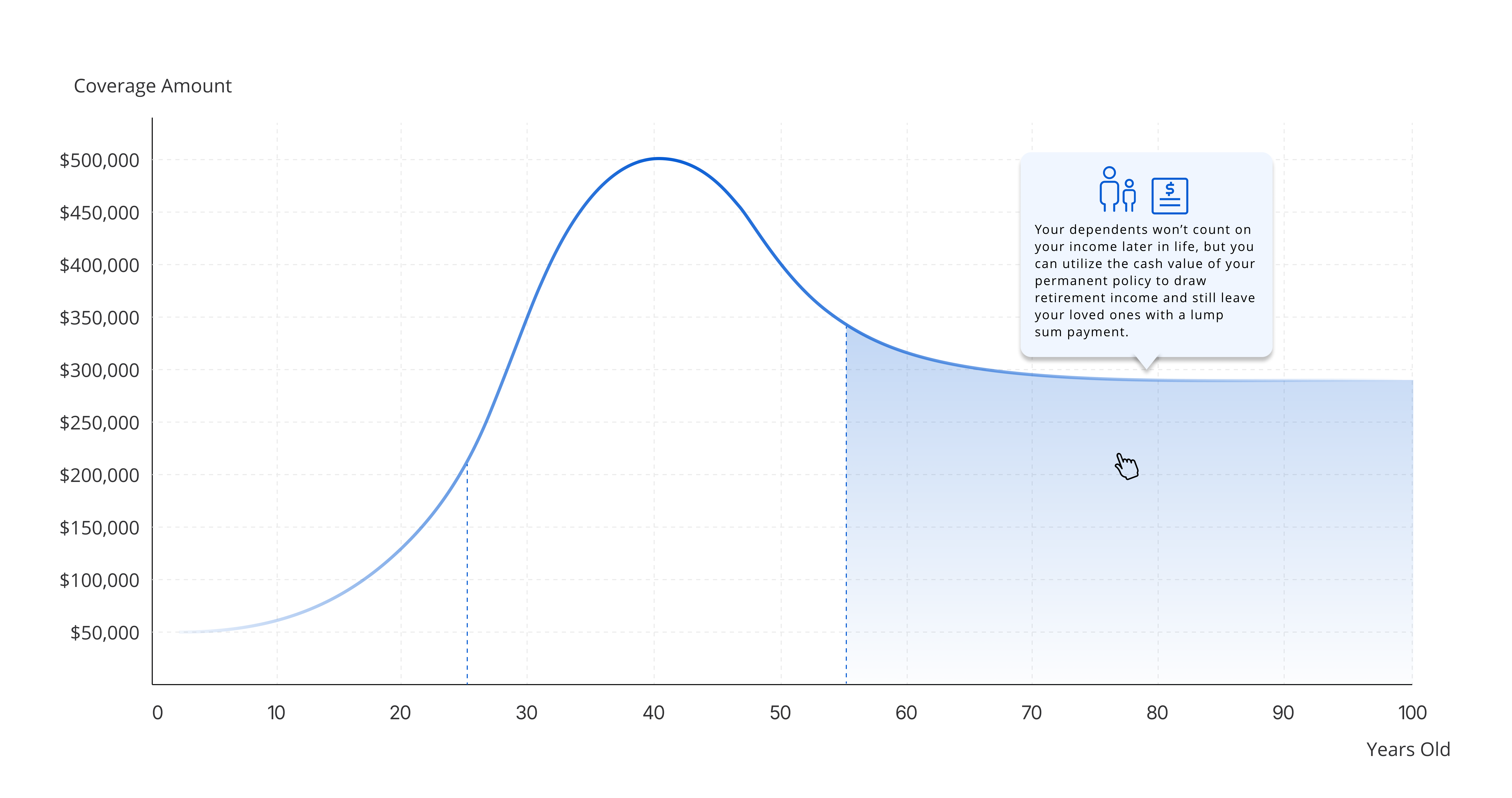

The amount of life insurance coverage you need can change over time.

You’ll want to consider…

Household Expenses

Ensure your family can maintain their current lifestyle by securing coverage for day-to-day expenses such as housing costs, utilities, groceries, and transportation.

College Expenses

Provide adequate financial support for your dependents’ education in the event of your death.

Outstanding Debts

Protect your loved ones from financial burdens like outstanding loans or credit card debts.

Medical Expenses

Safeguard your family’s financial security by ensuring there are funds available to cover medical bills, ongoing healthcare expenses, or potential long-term care needs.

End-of-Life Expenses

Cover the costs of your funeral, burial, or cremation to give your loved ones peace of mind in a difficult time.

So, how much life insurance coverage do you really need?

Meet Adam

Adam is 40 years old, he makes $65,000 a year, has a wife and two kids ages 7 and 11.

Adam wants to cover these expenses with his life insurance policy:

Now Here Is The Math…

How Is That Money Spent?

DIME Formula

The DIME formula is a common method used to determine how much life insurance coverage is necessary. DIME stands for Debt, Income, Mortgage, and Education, which are the four main factors that are considered when calculating life insurance coverage.

Once you have these four figures, add them together. This will give you a rough estimate of the life insurance coverage that you need.

Here’s how to calculate life insurance coverage using the DIME formula:

Debt

Add up all your debts, including mortgages, car loans, credit card balances, student loans, and any other outstanding debts.

Income

Determine how much income your family would need if you were to pass away. This includes both your current income and any future income that you would have

Mortgage

Calculate how much it would cost to pay off your mortgage in case of your passing.

Education

If you have children, consider how much it would cost to pay for their education, including college expenses.

The 10 Times Income Rule

Term vs Permanent Life Insurance

Term life insurance provides coverage for a specific period, usually 10, 20, or 30 years, and pays a death benefit if the policyholder dies during that term. It’s typically more affordable than permanent life insurance, but once the term expires, the coverage ends unless renewed or converted to a different policy.

Permanent life insurance provides lifelong coverage and includes a death benefit as well as a cash value component that grows over time. Unlike term life insurance, it remains in effect as long as premiums are paid, and the policyholder can borrow against or withdraw from the cash value while still alive.

Tips for Calculating Your Life Insurance Needs

- Remember that life insurance is an integral part of an overall financial plan. The amount you need should be based on factors like your income, debts, future expenses, and the financial needs of your dependents.

- Consider buying more than one policy to tailor coverage to your changing needs. This could look like supplementing a permanent policy with a term policy or specific life events like paying off a mortgage or funding education costs.

- Talk with your family about your needs to get a comprehensive understanding of the financial support they’ll require in your absence. This helps ensure the coverage aligns with your shared goals and responsibilities.

- Choose a life insurance policy with higher coverage than you think you need. This will allow for unexpected expenses or changes in your family’s financial situation.

- Reassess your policy regularly to ensure your coverage stays aligned with major life changes.

Ready To Take The Next Step?

The formula, multiplying your salary by 7, provides a solid beginning, but you don’t need to navigate this process by yourself. A life insurance expert from AmFi is ready to assist you in applying for the ideal type and amount of coverage. We’ll address all your questions, and identify the right life insurance plan that aligns with your budget and goals.

Life Insurance FAQ

Term insurance is a set amount of coverage for a set amount of time. Our term coverage is cost-effective and has a level premium. Once the term of your policy is up you will be required to re-apply for coverage. The coverage premium is calculated based on your current age, so don’t be surprised to see your term rates increase substantially if you choose to renew your term policy, assuming you’re still eligible for coverage. You can see if you qualify and apply for coverage online by clicking “Get a Quote”.

We believe term coverage is an inexpensive way for you to fill your insurance needs. However, the best form of life insurance coverage is permanent insurance. AmFi’s permanent policies provide lifetime level premiums regardless of age and medical changes. AmFi’s permanent policies also provide tax-deferred cash value growth. Contact our office or your local representative to learn whether permanent insurance is right for you.

Policies with AmFi start at $9 per month. The exact amount you pay each month (your premium) is determined by your choices in the coverage amount and length of term, as well as your age, health, and lifestyle choices.

No. With our 5, 10, and 20-year term policies you will be charged the same amount every month for the duration of your policy. When the policy expires, your rate may change based on age and insurability at that time.

We sure do. We don’t advise canceling your policy because your coverage will lapse, but if you cancel within the first 30 days, then we will issue you a full refund. If you cancel after the initial 30 days, then we’ll simply stop charging you.

In addition to life insurance coverage, this policy grows cash value that isn’t taxed right away. This cash asset is a tremendous advantage of our universal policies.

Please contact our office or one of our agents to discuss the universal life insurance policy and to see whether this is the best policy for your needs.

Just like with all our policies, the death benefit is completely tax free. The universal policies accumulate cash value that is tax-deferred. Please contact our team to learn more.

The Policy Owner must complete the appropriate form for the requested change. Forms may be downloaded and printed from the Forms Link after logging in. The Policy Owner may also contact a Service Representative at the Home Office or send us a message through our Contact Us page.

You may contact a Service Representative or register online. By registering online you will be able to view premium payments, make withdrawals and much more. Click here to register.

Upon the death of the Insured, you will contact the Home Office Claims Department to report the death. Be prepared to advise us of the insured’s name, the date and cause of death, and the name, address, and telephone number of the person who should be contacted. A Claimant’s Statement and additional information on how to file a death claim will then be sent to the named beneficiary(ies). You may click the “Claims” link at the top of this page to download the Claimant’s Form and instructions.

Please contact our office immediately to update your banking details and ensure that your valuable coverage isn’t lost.